“Every stage of life lays the foundation for the next stage of life. Treasure each stage.”

― Lailah Gifty Akita

The timing of when you buy life insurance is important.

Generally, the younger you are when you purchase life insurance, the less expensive it will be. As you age, coverage may become more expensive, or you could develop medical conditions disqualifying you from coverage.

Cheaper rates

The older you are, the more life insurance will cost because with age there are greater risks associated with health. This drives the premium cost for the same amount of life insurance benefit.

Juvenile life insurance

The parents or guardians of minor child often purchase juvenile life insurance policies. This insurance coverage can be purchased at birth and continue through high school and college, depending on the terms of the juvenile life insurance policy, and if the premiums are paid.

Juvenile life insurance normally has a smaller life insurance benefit, and the premiums are lower than adult life insurance.

If you are a parent or guardian, this may be an option you are able to add as a rider to your own life insurance policy. When the child matures and reaches the maximum age limit life for juvenile life insurance, the insurance will cease.

Life Insurance In Your 20s

When you decide to buy life insurance as a young adult in your 20s, you may be single and without children, and buying life insurance seems unnecessary. However, locking in a cheaper rate in your 20s can be a smart move, especially if you are buying whole life insurance.

Financial protection

Life insurance is primarily a benefit for those people in your life who would need your income should something happen to you.

If you have a spouse, children, or people who depend on you, having a life insurance policy may help them financially if you were to pass unexpectedly.

A term life insurance can be for 20 years, the time it takes to raise a child. A whole life insurance can last a lifetime.

A beneficiary might be your spouse, who would be responsible for loans, a mortgage, and caring for children.

If you don’t have children, but a two-income household, the surviving spouse may need financial protection if the other half was no longer contributing.

Life insurance in your 30s and 40s

In life, change is the one thing you can count on happening. Change can be positive and help us grow as individuals.

Change is unexpected, such as an accident or terminal illness can leave a spouse or family unprotected. Purchasing life insurance may help your family prepare for these unexpected changes.

There are frequent lifestyle changes in your 30s and 40s such as:

- Your career may be growing and advancing

- You may be going back to school to further your career

- You may be getting married or starting a family

- You may be buying your first home

- You start a new a business

These lifestyle changes may require responsibilities and assets to financially protect your family or business.

If you own a business solely or with a partner, a life insurance policy can help protect the business. The life insurance benefit can go to the partner for the benefit of the business. If you are a sole owner, the life insurance benefit can pay off any business expenses.

In your 50s and 60s – final expense insurance

Generally, you are still able to buy life insurance in your later years. A popular choice is purchasing a final expense insurance. This type of insurance acts like a term life insurance and is generally for a smaller benefit which may be enough to provide for funeral costs or other items.

A final expense insurance benefit can help offset extra expenses incurred with funeral cost or fees.

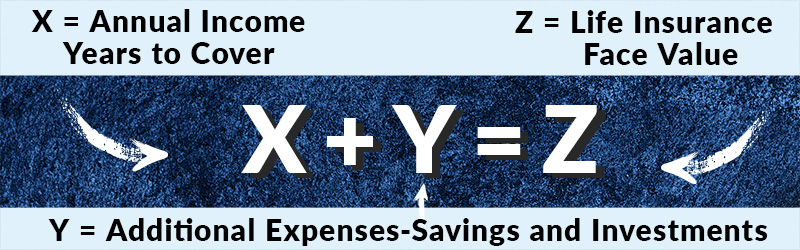

How much insurance do you need?

Depending on how much financial protection is needed for your family or future plans, some simple math can give you an idea:1

- Multiply your annual income by number of years needed to cover your family.

- Add additional costs to cover expenses such as a mortgage or college tuition

- Subtract the amount by how much non-retirement savings, investments or pension you currently have.

One of the best places to start a discussion of when you need to get life insurance is with a licensed life insurance agent. An agent can discuss your insurance options and help guide you.

Sources:

Reading Sources:

NAIC, https://content.naic.org/consumer/life-insurance.htm, accessed 2023.

Categories: Insurance, Life Insurance